http://www.asyura2.com/12/hasan78/msg/251.html

| Tweet |

JBpress>日本再生>日本経済の幻想と真実 [日本経済の幻想と真実]

日銀に責任を押しつける政治家たち

外債購入やインフレ目標で日本経済は回復するのか

2012年10月25日(Thu) 池田 信夫

不況が長期化する一方、財政赤字が積み上がって補正予算も組めない。こういう状況になると、中央銀行への政治的圧力が強まるのはどこの国も同じだ。

シカゴ大学のラグラム・ラジャンは「中央銀行はロックスターのように人気を集めている」と言うが、日本では逆に日銀は「無能な官僚機構」として政治家のバッシングを受けている。

しかし本当に日銀はできることをやっていないのだろうか?

日銀の外債購入は金融緩和ではない

前原誠司経済財政担当相は、記者会見で「日銀の外債購入のために日銀法改正を検討する」という方針を語った。政権の方針なのか、それとも(いつものように)彼の個人的な意見なのかはっきりしないが、「日銀による外債購入は金融緩和の手段として取り得る」という彼の話は、問題を取り違えている。

この外債購入という話は、日銀の国債購入にあまり効果がないことから、外債(特に米国債)を買うことでドル高(円安)にしようという話だ。これは為替レートを動かす効果はある。例えば日銀が数兆ドルの米国債を買えば、ドル高になることは間違いない。

しかしこれは前原氏の言う「金融緩和」ではなく、為替介入である。現在の為替介入は財務省が行っているが、実際のオペレーションは日銀がやっているので、違いはそれを外為特別会計ではなく日銀勘定でやるだけだ。

これは変動相場制では日常的に使う手段ではなく、為替の急激な変動を緩和するときに限って行うものだ。また日常的に行うことは、資金的にも不可能だ。東京外為市場だけでも1日に1兆ドル以上の資金が動いており、ドルを買い支えるには毎日、数兆円が必要である。

それによって為替差損が発生したら一般会計から補填しなければならないので、これは財政政策である。こんな大ギャンブルを税金で行うことは、賢明な政策とは言えない。

「非不胎化介入」は幻想だ

こういうとき、よくあるのは「日銀が外債を買って円を市場に供給すると、国内の金融緩和になる」という話だ。通常は、こういう副作用をなくすため日銀が円資金を回収する不胎化を行うが、資金を介入しない非不胎化介入を行うべきだ、と一部のエコノミストが主張している。

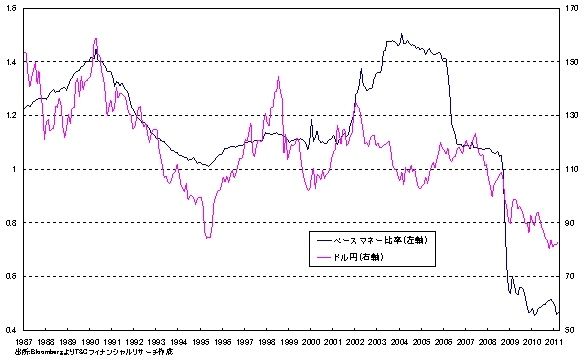

ソロス・チャート(出所:読売新聞)

拡大画像表示

これは一般論としては間違っていない。右の図は吉田恒氏が日米のベースマネー(中央銀行の発行する通貨量)の比率と為替レートを比較した「ソロス・チャート」だが、2000年頃までは両者はかなりパラレルに動いている。

しかし2002年以降、日銀が大幅な量的緩和を行った結果、日本のベースマネーはアメリカの1.5倍になったが、円は逆に高くなった。2008年の金融危機以降は、逆にFRB(連邦準備制度理事会)が激しく金融緩和したため、ベースマネー比率は半分以下になったが、為替レートはそれほど上がらなかった。

この原因は、日本の金利がゼロに貼りつく流動性の罠に陥ったからだ。政策金利もずっとゼロのままなので、日銀がそれ以上ベースマネーを出しても、市中に流通するマネーストックは変わらない。つまり流動性の罠に陥ったときは、為替介入はすべて不胎化介入だから、金融緩和の効果は期待できないのだ。

与党も野党も「万年野党」になった政治

他方、安倍内閣の官房長官を務めた自民党の塩崎恭久氏は、現代ビジネスで「政府と日銀は政策協調して一刻も早いデフレ脱却を! 日銀はモードを変え、『非伝統的』政策をも含め、あらゆる政策を総動員すべきだ」と書いている。

これも一般論としては間違っていないが、彼が「日銀がやるべき事は、『政策金利を下げる』か『予想(期待)物価上昇率を上げる』か『自然利子率を上げる』かのいずれかの政策」だと言うのは間違いである。

政策金利をゼロ以下に下げることはできないため、予想物価上昇率を上げることは日銀の政策として考えられるが、日銀が自然利子率を上げることはできない。自然利子率というのはインフレにもデフレにもならない(潜在成長率にほぼ等しい)金利のことで、実体経済で決まるから日銀はコントロールできないのだ。

前原氏も塩崎氏も、日銀がインフレ目標を設定するように日銀法を改正すると言う。私は努力目標の設定はしてもいいと思うが、それが実現できる保証はない。例えば1%というインフレ目標を設定すると、景気が過熱して2%になったら下げることはできるが、今のようにデフレ状態から1%にする政策は分かっていない。

要するに、これさえやれば日本経済の問題は一挙に解決するという「魔法の杖」はないのだ。金融政策の役割は景気変動を緩和することだが、今は景気が低迷したまま「低位安定」しているので、金融政策に大した効果はないというのが多くの経済学者の意見だ。

しかし政治家は、そんなことを言うわけにはいかない。だめと分かっていても、「日銀がやるべきことをやってないから景気がよくならない」と日銀に責任を転嫁すれば、何かやっているという格好をつけることができる。

それでも効果がないと、政治家は、永遠に「悪いのは日銀だ」と言い続けることができる。55年体制で社会党が「非武装中立」を唱えていたようなものだ。その社民党でさえ、図らずも政権に就いたら非武装中立をかなぐり捨ててしまった。

前原氏は、与党になっても「言うだけ番長」が抜けない。他方で自民党は、3年間ですっかり野党が身についてしまったようだ。与党も野党も「万年野党」になって無責任な政策ばかり唱える日本の政治は、劣化する一方である。

http://jbpress.ismedia.jp/articles/print/36393

政府と日銀は政策協調して一刻も早いデフレ脱却を! 日銀はモードを変え、「非伝統的」政策をも含め、あらゆる政策を総動員すべきだ

2012年10月23日(火) 塩崎 恭久

塩崎恭久レポート

海外の中央銀行関係者向けに日銀視察イベントを開き講演した白川総裁〔PHOTO〕gettyimages

48年ぶりに東京で開催されたIMF・世銀総会に合わせ来日した、銀行、投資銀行、ファンドなどの経営者、アナリスト達と意見交換をする機会に恵まれた。驚いたことに、最後の記憶が定かではないほど久しぶりに日本に対する視線が熱かった。

今なぜ日本に対する期待感が高まっているか、といえば、何も動かなかった過去3年間の経済政策の空白に区切りをつけ、漸く日本経済にも変化が起きそうだ、というのだ。

より具体的には、まず、民主党政権が終わり、安倍晋三新総裁率いる自民党が政権奪還し、大胆な成長戦略をとるのではないか、との期待が最も大きい。そしてほぼ同様に大きな期待がかけられているのは、来年4月の日銀総裁の交代だ。今度こそ本格的な積極的金融政策を断行し、デフレ脱却を図ってくれる人に替わるのではないか、という期待だ。

政府と日銀が政策協調して一刻も早いデフレ脱却を

安倍晋三総裁が自民党内に設置する「日本経済再生本部」が10月24日から本格稼働する。私も微力ながら事務総長代行として本部長である安倍総裁を支えていく所存だ。

安倍氏は総裁選を通じて、「一日も早いデフレ脱却と成長力の底上げで所得向上、雇用の創出に全力で取り組む」と成長戦略推進を訴え、経済を最優先課題とした。政府と日銀が政策協調して量的緩和に取り組んで行くべきだと主張し、日銀が背を向けるならば、日銀の強い独立性を規定している日銀法を再改正することを辞さないという強い立場すら、時に明らかにしてきた。

政府と日銀が政策協調して一刻も早いデフレ脱却を目指すというのは、今後の自民党の経済政策の柱になるだろう。この点、私も全く同意見である。そして、その協調する政策の中身は、政府も日銀も、「非伝統的」な政策、すなわち、これまでやったことのない政策をも大胆に導入しなければならないはずだ。

なぜならば、「失われた20年」に表れているように、日本経済の直面する問題は長期化しているうえ、最近の株価を見ても、欧米の株価水準がリーマンショック前の水準を1〜2割上回っているのに対し、東京の株価水準は依然としてショック前の7割程度の水面下にとどまっていることに見られるように、根深く、深刻だからだ。

要は、産業構造問題であり、競争力問題であり、そしてその根っこにある教育や規制、企業統治システムなどから来ている複合危機であり、根本解決は並大抵ではない。

日銀法上の目標は何も達成できていない

日銀の使命は何か。日銀法の第2条にはこう書かれている。

「日本銀行は、通貨及び金融の調節を行うに当たっては、物価の安定を図ることを通じて国民経済の健全な発展に資することをもって、その理念とする」

ではこれまでの日銀はその理念を達成しているか?

第一に「物価の安定」だが、消費者物価は持続的に下落しており、失格だ。一方、国内総生産(GDP)も縮小が続いており、とても「国民経済の健全な発展」とは程遠く、これまた失格であり、結局、日銀法上の目標は、現在の日銀の下では、いずれも達成できていない。

成長率や物価上昇率がマイナスになれば、政策金利を「マイナス金利」とすることは不可能であることから、財市場での均衡をもたらす名目金利(自然利子率)より政策金利の方が高い状態が続くことになる。つまり、金融緩和が不十分ということになるわけだ。

論理的には、日銀がやるべき事は、「政策金利を下げる」か「予想(期待)物価上昇率を上げる」か「自然利子率を上げる」かのいずれかの政策、もしくはそうした政策の組み合わせということになる。

量的緩和が不十分であるという認識に欠けている

政策金利をマイナスにできないため、実質的な政策金利をこれ以上引き下げるには、量的緩和を大胆に行うしかない。日銀総裁が「無条件緩和」を宣言するなど、市場に強いメッセージを発することが必要だ。また、長期国債の巨額購入や、様々な資産の大量購入など、まさに「非伝統的金融政策」にまで踏み込むことが大事だ。為替も円安に向かう筋合いだ。

予想(期待)物価上昇率を上げるには、きちんとした物価上昇率目標を設定することだ。いわゆる自ら設定するインフレターゲットである。安倍総裁は2%程度を示唆している。ただし、ここで重要なことは、目標を掲げたら、それを必死で達成しようとしている「本気度」を市場に伝えることである。

これまでの日銀は、例えば本年春のように、市場が日銀の緩和に向けての真意を疑うようなマネー供給の不十分さや目標達成への決意に水をかけるような総裁発言があってはならず、中央銀行総裁は、「偉大なるコミュニケーター」で居続けなければならない。

一方、財市場の均衡金利を上げるには、生産性向上、企業再編、雇用促進等への融資優遇制度や、財政面でもこれまでやったことのない「非伝統的」な産業構造転換、競争力強化策を集中導入していくしかない。

例えばiPS細胞研究でノーベル賞を受賞された山中教授の研究に追加予算を付与するなど研究開発支援の徹底、大学・大学院改革の推進、加速度償却、さらには、「法人税等ゼロ特区」の全国展開、「東京一極集中解消税制」創設といった投資優遇税制などである。

ところが、日銀を見ていると、量的緩和が不十分であるという認識に、欠けているとしか思えない。日銀はデフレ克服に国債の購入といった量的緩和は効果が薄いと主張する。だが、日銀総裁が「とことんやる」というメッセージを市場にきちんと出すだけでも、デフレ脱却への道が開かれると思う。今は総裁と市場との対話が欠如していると言うほかない。

「非伝統的」政策をも含め、政策を総動員すべき

白川総裁は今年4月21日に行った米国のワシントンでの講演で、「中央銀行の膨大な通貨供給の帰結は、歴史の教えに従えば制御不能なインフレになる」と述べた、という。長引くデフレへの世の苛立ちを踏まえると、何とも間の悪い発言だった。そして今でも総裁の本音は同様と見られている。

さらに日銀が実施してきた量的緩和姿勢が、戦力の逐次投入的なやり方に終始した上に、何よりも説明がうまくなかった。国内外の市場や経済界、そして国民からの信頼をすっかり失ってしまっている。日銀の独立性が尊重されるには、国民からの「信頼と信認」が不可欠だが、日銀はそれを失っている。だから、与野党を問わず日銀法改正の声が高まる一方なのだ。

経済が低迷しているときに消費税率を引き上げても、経済を一層冷え込ませ、同時に肝心の税収が増えないことはすでに証明済だ。1997年に税率を3%から5%に上げた際、所得税の引き下げとセットにしたため、税収的には中立なはずだった。ところが税率引き上げ前に54兆円あった税収は翌年50兆円を切ったのである。以後15年間、産業構造転換が全く不十分ゆえに競争力を失い続け、未だに当時の税収にすら追いついていない。

前回の安倍政権では日本経済の構造改革を推し進めることで、成長を目指した。その結果、日経平均株価は1万4,000円台から1万8,000円台に上昇、税収も51兆円まで増えた。それが21世紀に入ってからの最大の税収である。

白川総裁の5年間の任期は来年4月までである。残り半年。与野党に広まる日銀法改正の声を前に、デフレをきちんと克服した総裁として歴史に名を残すためには、法改正の前にまだまだやれる事がある。日銀はモードを変え、「非伝統的」政策をも含め、あらゆる政策を総動員すべきだ。市場と向き合って経済発展に向けて、思い切り明確なメッセージを出すことが何よりも大事だ。日銀にとってラストチャンスだし、それはほとんど日本経済にとってもラストチャンスと言ってもいい。

現総裁にその気がないままでは、来年4月の後任人事で、柔軟で、政府とも、市場とも、国民とも、世界とも対話を行い、経済の健全な発展を真に追及しようとする人を選ぼう、ということになろう。そして、それでもダメとなって日銀法改正に突入することは、先進国の矜持として、絶対避けたいものだ。

http://gendai.ismedia.jp/articles/-/33862

Raghuram Rajan

Raghuram Rajan, Professor of Finance at the University of Chicago Booth School of Business, served as the International Monetary Fund’s youngest-ever chief economist and was Chairman of India’s Com…

Full profile

Oct. 19, 2012

CommentsTOKYO – What should central banks do when politicians seem incapable of acting? Thus far, they have been willing to step into the breach, finding new and increasingly unconventional ways to try to influence the direction of troubled economies. But how can we determine when central banks overstep their limits? When does boldness turn to foolhardiness?

Illustration by Jon Krause

CommentsCentral banks can play an important role in a cyclical downturn. Interest-rate cuts can boost borrowing – and thus spending on investment and consumption. Central banks can also play a role when financial markets freeze up. By offering to lend freely against collateral, they “liquify” assets and prevent banks from being forced to unload loans or securities at fire-sale prices. Anticipating such liquidity insurance, banks can make illiquid long-term loans or hold other illiquid financial assets.

CommentsTo the extent that unconventional monetary policy – including various forms of quantitative easing, as well as pronouncements about prolonging low interest rates – serves these roles, it might be justified.

CommentsFor example, the US Federal Reserve’s first round of so-called quantitative easing (QE1), implemented in the midst of the crisis, was doubly effective: By purchasing mortgage-backed securities, the Fed brought down interest rates in that important market (in part, probably, by signaling its confidence in those securities), and restored it to vitality. Similarly, with its outright monetary transaction (OMT) program, the European Central Bank has offered to buy peripheral eurozone countries’ sovereign bonds in the secondary market – provided that they sign up to agreed reforms.

CommentsThe logic is that conditionality will ensure that countries are solvent, while OMTs will restore trust to a market that has broken down because investors fear that the countries concerned will exit the eurozone. Again, its effect, thus far, has been significant.

CommentsOther unconventional policies, however, have been undertaken to stimulate the economy, rather than to deal with broken markets. The benefits have been commensurately smaller. QE2, in which the Fed bought long-term government bonds, did not have a discernible effect on long-term government interest rates. Indeed, with its recent decision to pursue QE3, the Fed is focusing once again on the mortgage-backed securities market; but, given that the market is much healthier now, it is unclear how much good this will do.

CommentsRecently, the Fed expressed its intent to keep policy rates low for a long time – until employment picks up strongly. The hope is that if investors consider this announcement credible, long-term interest rates will come down further, encouraging spending. But the immediate effect on long-term bond rates has not been encouraging.

CommentsAs central banks venture farther into uncharted territory, advocates argue that at worst they will do no harm. In fact, no one really knows.

CommentsFor example, sustained low interest rates hurt savers who traditionally prefer safe short-term investments. Pensioners and those near retirement, facing low income from interest, may cut back further on consumption, weakening the economy. Bolder pensioners, desperate to generate higher returns, may take undue risks – for example, investing in junk bonds – that could jeopardize their nest eggs. And, unfortunately, such financial risk-taking may have little impact in terms of spurring corporations to assume more risk by investing.

CommentsSimilarly, a potential downside to quantitative easing is that low interest rates send capital to higher-growth, high-interest-rate countries. In theory, as capital floods in, these countries’ exchange rates will appreciate rapidly, making them look unattractive and automatically stemming the flow. In practice though, as investors make money on their trades, they bring in yet more money, forcing further currency appreciation. All too often, the process does not end smoothly but in a crash. No wonder recipient countries resist inflows of hot capital.

CommentsWe also know little about how smooth the exit from quantitative easing will be. In theory, as the economy picks up and interest rates begin to climb, central banks will simply pay higher interest rates on their reserves, so that they can finance their holdings of long-term securities and shrink them slowly. But higher interest rates also imply large capital losses for central banks’ asset holdings.

CommentsEven if some of these losses are offset for the government as a whole (as the central bank loses on its holdings of government debt, the treasury gains in equal measure, because the debt it owes is worth less), the losses on long-term private debt holdings are real. Moreover, the argument that losses are offset is not easy to explain to the public. Will opinion be sympathetic to the Fed when politicians like Ron Paul excoriate it for losing tens of billions of dollars monthly on its asset holdings? Will bond markets fall sharply (and interest rates rise) as markets fear that the Fed will be pushed to sell its enormous holdings in short order?

CommentsA last defense offered by advocates of continuing on the path of adventurous monetary policy, even when the perceived benefits are small, is that, because politicians refuse to settle their differences and act, monetary policy is “the only game in town.” In democracies, when there are no other alternatives, politicians often eventually do the right thing. By creating the impression that something beneficial is being done, unconventional monetary policy relieves pressure on politicians. So, when central bankers argue that they are the only game in town, they are ensuring that outcome.

CommentsCentral bankers nowadays enjoy the popularity of rock stars, and deservedly so: their response to the difficult and uncertain environment during and after the financial crisis has been largely impeccable. But they must be able to admit when they are out of bullets. After all, the transformation from hero to zero can be swift.

Reprinting material from this Web site without written consent from Project Syndicate is a violation of international copyright law. To secure permission, please contact us.

Share this

inShare

New commentFilterExplain this

Comments (5)

You need to login in order to leave a comment. If you do not yet have an account, please register.

100%

Zsolt Hermann Yesterday

Unfortunately the whole situation is upside down.

The central banks, or any bank in fact should not play any role in what is happening.

The banks simply got into their prominent positions as a result of the excessive, constant growth economy forcing everybody into overspending, relying more and more on credit.

But these financial institutions, with their inflated and imminently bursting bubbles have no real bullets at all, they have absolutely no capacity to solve the crisis, it is the opposite, with this meddling, pouring virtual money into the tanks of the broken system, "providing false liquidity" they delay the "revelation of the evil", the recognition of the true problem which is the basic economic model and its serving cast.

The banks should gradually withdraw from the arena leaving leaders and public to examine and understand how a global, interdependent human network works in a closed and finite natural system, and what new socio-economic model is suitable to provide a predictable and sustainable future.

Expand

Frank O'Callaghan 5 days ago

We must recognize where the problem began. The quest for widening inequality has created instability. Huge personal remuneration in the financial sector coupled with the refusal to honestly account the zero sum game of paper shuffling built up unacknowledged deficits that were hidden by less and less credible rouses until the fall of Lehman Bros.

The crisis of confidence has caused doubt in the values of many asset classes. The ocean of liquidity poured by central banks has been taken by the very criminals who caused the problem rather than being used to prime the pump of international trade in the real economy.

So, what is our solution? Clearly the bill must be paid by those who caused it. The great wealth of the beneficiaries of the crisis should be immediately forfeit. Inequality must be narrowed or eliminated. Power, work, resources and responsibilities must be more broadly shared. Unemployment must be brought down to an acceptable 2-4% of the workforce and special attention paid to the long-term unemployed.

Our world has great challenges ahead, not least in environmental and demographic terms. We have tools to hand that are much more powerful than the merely economic. We must begin to use them.

Expand

PROCYON MUKHERJEE 5 days ago

Raghuram is once again back at his best!

Unfortunately the game is not only the only one, it could well be the everlasting one (QE infinity); one would find the argument perfectly ludicrous that firstly the money would ensure that asset prices would inflate and then it would make ‘some’ wealthy and then this incremental ‘wealth effect’ would make people spend more thus creating jobs!

Those markets that shadow future expectations like stocks and commodities have met with a mixed reaction; after the initial euphoria the markets would have better sense prevailing that such high PE multiples with such low fixed asset investment is untenable, while the corporate sector would keep importing jobs.

It leaves a sobering thought that with fiscal cliff-hanger in play and the quality of public investments deteriorating over time and with a looming bubble of debt which is growing with such ferocity, what does it leave FED, when the interest rates eventually harden and unwinding actions knock on the door? Or are we assuming that interest rates have no other way to go, which if true defeats the very purpose of the stimulus as then we are projecting a continuation of low job growth environment and perpetual low inflation?

Procyon Mukherjee

Expand

captainjohann Samuhanand @captainjohann 5 days ago

The politicians of India have been clamoring for a loosening of its tight monetary policy which the Indian Central bank is following.They have milked the Indian public sector banks like State bank etc to give loan to unscrupulous Indian big fat cats like Mallaya who sits on real estate worth crores but takes loans to pay CEOs who donot pay his pilots and staff.Same with some of the other Indian big fat cats who milk the Indian savings through corrupt politicians and now NPA(non performing assets) of Indian public sector banks is worrying.

Expand

srinivasan gopalan @geeyes34 5 days ago

With his characteristic clarity, the distinguished professor has done a nice job in highlighting the risks embedded in pursuing unconventional monetary policy, particularly in the United States. The deliberate attempt to keep the interest rate at flat or zero with a view to reviving consumption and stoke the demands for funds by the stakeholders by the Federal Reserve cannot be replicated in other countries which have their own peculiar problems. For instance, Dr Rajan, who is currently the Chief Economic Advisor in the Finance Ministry of India, cannot get around the country's apex bank, the Reserve Bank of India, to experiment with unconventional monetary policy. Even otherwise, calls from the authorities quite often signal indirect message to the RBI to change gear for a cut in policy rates. Though trade and industry in India have been demanding policy rate cuts to help them generate growth impulses and to stay invested in downturn times like this, the RBI is not flinching from its fixed goal of taming inflation which is relentlessly going up. It would be a travesty of policy for the central bank in India if it is to follow the example of the Federal Reserve to flood the money market through a cheap money policy. It is nice to know that Dr Rajan is not even overly enthusiastic about countenancing such a policy in the US, though it had not caused major damage to its economy so far. But in an uncertain milieu like this, it would be imprudent to break from convention and resort to magic bullet lest the results should come home to roost before long, much to the dismay of the stakeholders of the real sectors of the economy. G.Srinivasan, Journalist, New Delhi (India)

Expand

http://www.project-syndicate.org/commentary/the-limits-of-unconventional-monetary-policy-by-raghuram-rajan

吉田恒の為替予想

「1ドル60円」示唆するソロス・チャート

4月にかけて起こった急激な円安・米ドル高は85円台で一息つきました。それはある意味で当然でしょう。為替など相場は実態経済の変化を先取りして動く傾向がありますが、別な言い方をすると、実態経済自体はそう簡単に変わらないからです。

たとえば、あの3月に76円台まで進んだ円高・米ドル安の原因は何だったでしょうか。1つのポイントは、米国の空前の金融緩和を受けて米ドルが「じゃぶじゃぶ」に溢れたということでしょう。

下のグラフ「ソロス・チャート」(注)は、日米中央銀行の資金供給量の差(ベースマネー比率)と米ドル円の関係を見たものです。これをみると、日米の資金供給量の差が空前の「米ドル余り」となり、その中で円高・米ドル安が広がってきたことがわかるでしょう。

ソロス・チャート

3月の東日本大震災などを受けて、日銀も一段の資金供給拡大に動いたものの、空前の「米ドル余り」は、このグラフを見る限りまだ顕著な変化はありません。「米ドル余り」は、米ドル円が60円程度の円高・米ドル安になる可能性を示唆しています。それは震災前後で大きく変わっていないのです。

相場は先取りするものです。――空前の「米ドル余り」に変化がなくても、この先、まだ日銀が円を「じゃぶじゃぶ」にする状況が続くだろう。一方で米国は出口戦略で余った米ドルの回収に動くだろう――そういった予想から、「米ドル余り」が変化することを見越して、米ドル買い・円売りに動くのはわからなくはありません。

ただし、実際の経済状況の変化は遅れてついてくるので、相場の先取りは何度か失敗を繰り返すのが普通です。その中で、本当に円高から円安へ中長期の基調が変化したのかを試すことになっていくのです。

(注)為替市場の代表的な参加者であるヘッジファンドが、かつてこの日米中央銀行の資金供給量の差と米ドル円の関係に注目し、話題になったことがあったことから、ヘッジファンドの有名人、G.ソロスの名前から「ソロス・チャート」と呼ばれています。

プロフィル

吉田 恒(よしだ・ひさし)

1962年、青森県生まれ。85年、立教大学文学部卒業後、自由経済社(現・T&Cフィナンシャルリサーチ)入社。同社代表取締役社長。投資情報事業を展開するT&Cグループの持ち株会社・T&Cホールディングス取締役などを歴任。2011年7月から、米国を本拠とするグローバル投資のリサーチャーズ・チーム、「マーケット エディターズ」の日本代表に就任。国際金融アナリストとして、執筆・講演などを精力的に行う。FX会社が主催する投資教育プロジェクト、「FXアカデミア」の学長も務める。

<主な著書など>

「さよなら円高」「YENの悲劇」(ともに廣済堂出版)、「投資に勝つためのニュースの見方、読み方、活かし方」(実業之日本社)、「FX7つの成功法則」(ダイヤモンド社)、共著に「通貨大動乱」(総合法令)、DVDに「こうすればFX予想は当てられる!」(パンローリング)がある。

(2011年4月26日 読売新聞)

FXのリスクについて

※FXは証拠金額より大きな額の取引が可能なことから、外国為替相場や金利水準の変動によって損失を被る可能性があり、その損失の額が証拠金額を上回ることがありますので、ご注意ください。

※本企画で紹介している企業各社の商品についてのメリット・リスク・手数料などの詳しい内容や個人情報の取り扱いについては、各社ホームページの該当ページにて、ご自身でご確認ください。

無料でFX口座を開設できる大手FX会社の情報が満載 ⇒ ヨミウリ・オンライン特設ページへ

関連記事・情報

Powered by popIn

【マネー・経済】ドル円を支配するチャート (2011年12月13日)

【マネー・経済】知られざる介入成功の鍵とは? (2011年11月8日)

【マネー・経済】人気の豪ドルが急落した理由 (2011年10月4日)

【マネー・経済】ドル高40日目はどんな感じ? (2011年5月17日)

【マネー・経済】東日本巨大地震、国難相場へのヒント (2011年3月14日)

http://www.yomiuri.co.jp/atmoney/fx/forecast/20110426-OYT8T00512.htm

|

|

|

|

この記事を読んだ人はこんな記事も読んでいます(表示まで20秒程度時間がかかります。)

|

|

スパムメールの中から見つけ出すためにメールのタイトルには必ず「阿修羅さんへ」と記述してください。

スパムメールの中から見つけ出すためにメールのタイトルには必ず「阿修羅さんへ」と記述してください。すべてのページの引用、転載、リンクを許可します。確認メールは不要です。引用元リンクを表示してください。